Most acquisition conversations skip the most important question: what happens to the person who built the thing?

Do founders stay after selling their company? The honest answer is — it depends entirely on why they sold and what the buyer actually needs. There’s no universal answer, but there are three clear models I’ve seen play out repeatedly when we acquire businesses at Vangal.

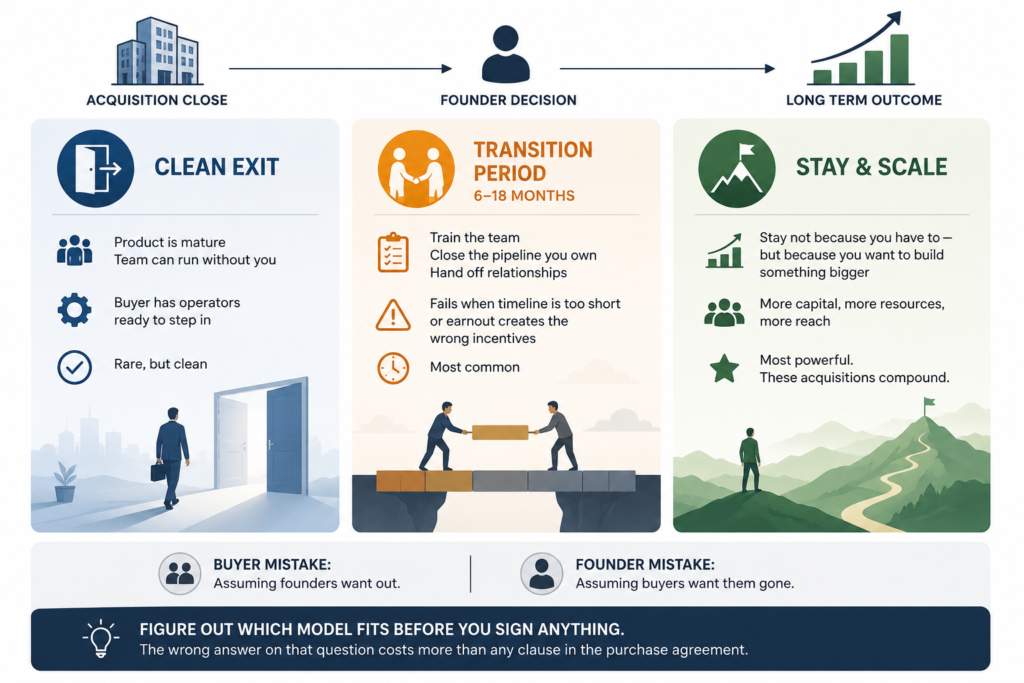

Model 1: The Clean Exit

Some founders are done. Burned out, ready to move on, or selling precisely because they don’t want to run the business anymore. This is more common than buyers admit.

A clean exit means the founder leaves within 30-90 days. They document processes, hand over relationships, and walk away. The buyer needs to have operational infrastructure ready to absorb the business immediately — or it falls apart fast.

We’ve done clean exits at Vangal. They work when the business has strong systems, a capable second-in-command, and customers who aren’t relationship-dependent on the founder. If none of those three exist, a clean exit is a risk you’re underwriting on day one.

Model 2: The Transition Period

This is the most common structure. The founder stays six to eighteen months, earns an earnout tied to performance, and transfers institutional knowledge gradually. It’s the default in most small SaaS and agency acquisitions.

The problem is that “transition period” means very different things to different people. To the founder, it often means “I’ll answer questions.” To the buyer, it means “you’ll run the business while I restructure it.” That gap kills deals post-close.

When we structure transitions at Vangal, we define deliverables explicitly — not just duration. Which customers get a warm introduction. Which systems get documented. Which hires the founder helps recruit. Vague transitions create resentment and churn on both sides.

Model 3: Stay-and-Scale

The most underrated outcome in micro-PE. The founder rolls equity, takes a leadership role, and builds the business under a new ownership structure with actual resources behind them. This is what do founders stay after selling their company really looks like at its best.

This works when the founder is still hungry but constrained — undercapitalized, isolated, or stuck wearing too many hats. They don’t want out. They want leverage. A PE firm that understands operations can provide that.

Stay-and-scale only works if the founder and acquirer align on the vision for what the business becomes. If the buyer wants to cut costs and harvest cash flow while the founder wants to build a category leader, it will fracture. We screen for this alignment hard before we close.

What Actually Drives the Outcome

Three things determine which model plays out. First: founder motivation. Are they selling to escape, to unlock capital, or to accelerate? Each produces a different post-close posture.

Second: business dependency. How much of the revenue, relationships, and product knowledge lives in the founder’s head? High dependency means the buyer needs the founder to stay whether they want to or not. Low dependency creates optionality.

Third: deal structure. Earnouts keep founders engaged. Clean cash-at-close creates clean exits. Equity rollovers create partners. The financial terms signal what both sides actually want — and they shape behavior accordingly.

When people ask do founders stay after selling their company, they’re usually asking the wrong question. The better question is: what structure actually aligns incentives for what comes next? Get that right and the retention question answers itself.

The founders who regret selling are almost always the ones who didn’t negotiate for the role they actually wanted post-close. Don’t let the transaction define what happens after it.